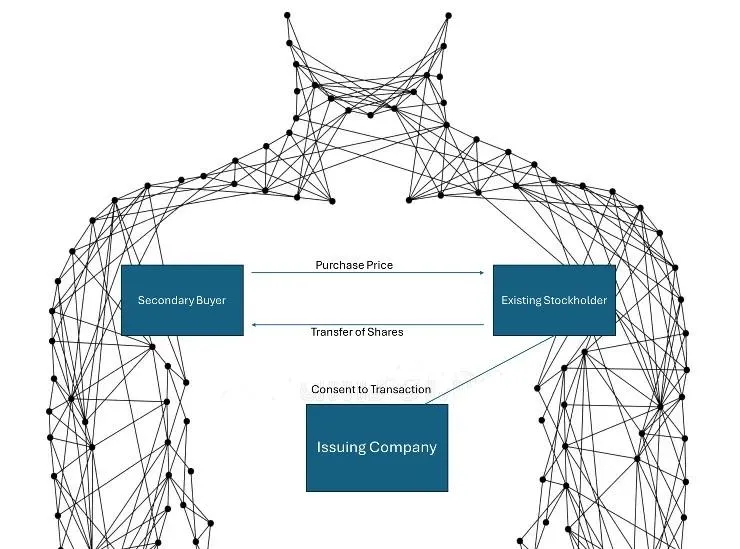

Anatomy of a Secondary Sale

With no guaranty of subsequent financing rounds and limited opportunities for exit in the venture capital market, the uptick of secondaries in 2024 (an estimated more than $100 billion in deal volume) makes sense. Our experience in the last year is consistent with that trend - we have seen an uptick in secondaries activity from our clients. Below is an example transaction, based on deals we’ve closed in one form or another a few times in recent years.

The Scenario

A founder (“Remaining Founder”) of a Series Seed startup approaches us to structure a Buyout of his co-founder (“Departing Founder”)’s equity and its sale to a third party (“Secondary Sale”). They both agree to part ways due to irreconcilable differences in how they want to operate the business. The Remaining Founder also see this as a liquidity opportunity and would like to include some of his own shares in the Secondary Sale.

Besides resolving the founder conflict and providing liquidity, the Secondary Sale also would allow the Remaining Founder to bring in a third-party buyer that provides strategic value (a “Strategic Buyer”). The Strategic Buyer often is an emerging VC - an emerging fund manager or family office - with expertise, relationships, or a passion for the Company’s industry or business. How do we approach this transaction?

The Execution

This kind of Buyout and Secondary Sale requires us to maneuver several issues, including:

Valuation: The board should work with the Company’s financial advisors to determine pricing of the Secondary Sale. Secondary transactions can affect a company’s valuation, especially if they lead to inconsistent pricing across different sales. This can complicate future fundraising and impact employee stock options. In the examples we have seen, the Company in question was indeed planning on a Series A in the near future. The Strategic Buyer, of course, will negotiate this purchase price.

Regulatory: Legal helps confirm that the Secondary Sale is structured to comply with securities laws, particularly the Securities Act of 1933. This analysis includes confirming that sellers are not deemed underwriters and that the Secondary Sale qualifies for exemptions from registration.

Consents and Approvals: A Seed stage company has already raised some outside capital and this has to comply with the various approvals/consent rights built into its governing documents and its agreements with its Series Seed investors.

Board Consents: In our example, the board has to approve the repurchase of all shares owned by Departing Founder. That is, under the Company’s governing documents, the Company’s right to repurchase a portion of the Departing Founder’s shares depends on a board finding that certain factual conditions had been met. The board also has to approve the re-sale of those shares (along with some held by the Remaining Founder) to the Strategic Buyer, and set the price.

Stockholder Ratification: Since the Remaining Founder both sits on the board and is participating in the sale, we advise the client to ratify the interested party transaction under Section 144 of the DGCL. To that end, we draft a consent for the stockholders owning a majority-in-interest of the Company to sign affirming that they find the terms fair and in the Company’s best interests.

Series Seed Major Purchaser Consent: As is common, the Series Seed documents grant the Major Purchaser in that round a consent right over the Company’s repurchases of shares. The Company’s governing and Series Seed documents also grant a right of first refusal (ROFR) to the Company, first, and to the Major Purchaser, second, in any sale of shares by the Founders. Since the Company is partially waiving its ROFR, we still have to obtain the Major Purchaser’s waiver of its ROFR to allow a sale of the shares to a third party instead.

Transaction Documents: Once we navigate compliance, consents and approvals, executing the actual transaction often proves relatively straightforward. The main transaction document is a stock purchase agreement - more complex than the purchase agreement startup founders usually sign for their initial equity, but far less complex than the purchase agreements . Much of the work at this stage is deciding with the third-party purchaser and their counsel where the agreement will ultimately land on the limited reps, warranties, and indemnification provisions in the agreement. When there are multiple purchasers in the secondary round, we also sometimes negotiate side letters, granting certain special rights to strategic/bigger check purchasers.

Disclaimer. The contents of this article should not be construed as legal advice or a legal opinion on any specific facts or circumstances. Your viewing and/or use of the contents of this article do not create an attorney-client relationship with Cadet Legal. The contents are intended for general informational purposes only, and you are urged to consult with counsel concerning your situation and specific legal questions you may have.